1. Review of the performance of major assets this month

A-share market: In April 2017, according to the equity market monitoring model:

Market performance: The Shanghai Composite Index fell 2.11%, the small and medium-sized board and the ChiNext fell 1.56% and 2.79% respectively. The A-share market entered the downtrend channel in mid-April, ushered in a small rebound at the end of the month; April Wandequan A The overall valuation fell to 20.21 times. The valuation of the Shanghai Composite Index, the Shanghai and Shenzhen 300, and the small and medium-sized board is close to the median. The valuation of the GEM is gradually moving downwards. The relative valuation with the Shanghai and Shenzhen 300 has dropped to about 4 times. It is expected that the valuation of non-ferrous metals, petroleum and petrochemicals and coal sectors has been greatly reduced in the case of overall decline in bulk commodities, and the valuation of the banking sector has been adjusted in the context of the strict supervision of the CBRC.

Market style: During the period, the index volatility of the small and medium-sized styles rose slightly, and the volatility of the market style index fell. The industry index closed almost across the board, with non-bank finance, transportation, food and beverage, home appliances and other industries falling less; Bloomberg A shares The style factor model shows that only the profit factor and the scale factor have a positive monthly yield, indicating that the large-cap stocks are resisting the decline in the smaller channel.

Market liquidity: During the period, the accumulated outflow of funds exceeded 50.1 billion yuan (excluding the bank certificate), the total number of new shares issued was 20.813 billion yuan (based on the date of listing), and the net inflow of the bank account three weeks before the transfer was 7.8 billion yuan. The net inflow of shares was positive, and the ending balance of securities trading settlement funds rebounded to a high level since the beginning of the year.

Market sentiment: Market sentiment has rebounded this week. The turnover rate and financing purchases rebounded slightly in March. The derivatives market was generally neutral. The central value of the stock index futures basis was basically unchanged, and the IVIX index average decreased slightly. The number of new investors in March exceeded the total of January and February, but the first two weeks of April fell by about 50% from the same period in March.

Behavioral signals: This week's behavioral signals indicate that investor behavior is weak. In terms of industrial capital, the reduction in holdings has declined but remained positive. In terms of institutional investors, both public and private placements have declined, while for individual investors, the monthly average of the balance index has risen.

In this issue, the A-share market trend was high and low. Xiong'an New District, Guangdong, Hong Kong, Macao and Dawan District, and the “Belt and Road†boosted the market. Geopolitical factors drove the military to strengthen, but then the regulatory authorities demanded that the relevant concept stocks be suspended from self-inspection. At the same time, the introduction of regulatory policies for sub-new shares and high-transfers has curbed the market activity of the previous accumulation. Under the situation of global risk events, risk assets underperformed, and European and American stock markets also suffered a correction, and demand for safe havens was highlighted.

The recent over-regulation of financial markets has caused disturbances in liquidity and market sentiment. Since March, the China Banking Regulatory Commission has focused on the implementation of special treatments such as “three violationsâ€, “three sets of benefits†and “four impropersâ€, in the article “Regulations on the regulation of arbitrage, arbitrage and arbitrage, and related arbitrage in banking financial institutionsâ€. Non-bank institutions will use extra-budgetary funds to leverage leverage, increase duration, and add risk as “freewheeling†of wealth management; the CSRC issues “Institutional Supervision Reportâ€, clarifies the relevant regulatory requirements for institutional custom funds, and gradually strengthens Investigation and handling of illegal acts in new stock transactions and substantial supervision of company listing, delisting and mergers and acquisitions. A series of strict policies have triggered concerns about liquidity risks in the short term. Under the financial environment of “strict supervision, stable currency, and leverageâ€, we believe that radical deleveraging will not appear, and the negative marginal utility caused by regulation will gradually Regression, a round of valuation after the oversold repair market can be expected.

|

![[Monthly report - financial futures] The net value of the portfolio is slightly retraced, and the CVaR portfolio performs better.](http://i.bosscdn.com/blog/fc/0f/d8/0d8b64b3a83d529ce405c00739.jpg)

|

![[Monthly report - financial futures] The net value of the portfolio is slightly retraced, and the CVaR portfolio performs better.](http://i.bosscdn.com/blog/3d/65/22/eaf5168c486cd4d63d5b779e09.jpg)

|

![[Monthly report - financial futures] The net value of the portfolio is slightly retraced, and the CVaR portfolio performs better.](http://i.bosscdn.com/blog/d9/ee/84/f15569e7f4d3a6e991a2587aa9.jpg)

Bond Market:

In April 2017, the central bank passed a total of 880 billion yuan in reverse repurchase through 7 days, 14 days and 28 days. The total amount of funds returned was 670 billion yuan, and the net purchase of reverse repurchase was 210 billion yuan. The central bank on April 17 The delivery of 367.5 billion yuan of December MLF and 128 billion yuan of June MLF, on April 13 and 18, a total of 451.5 billion yuan of June MLF expired, MLF net delivery of 44 billion yuan; the current open market operations total net delivery 254 billion yuan.

Near the end of the month, the liquidity of the money market showed the characteristics of “near tightness and far-reaching pineâ€. The 1-day and 7-day silver deposit pledged repo rates rebounded compared with the beginning of the period, and the rest of the varieties were roughly the same as the beginning. Shibor's interest rate for various maturities also met this characteristic. On April 28, Shibor was 2.8190% overnight, higher than the April average of 25.83 basis points, and Shibor was 2.8699% for one week, higher than the April average of 12.18 basis points.

Treasury yields rose sharply, with a one-year period of 3.1672%, an upward 30.40 basis points, a three-year period of 3.2298%, an upward trend of 21.12 basis points, a five-year period of 3.3417%, an upward trend of 26.35 basis points, and a seven-year period of 3.4696%. Up 24.24 basis points, 10-year period is 3.4688%, up 18.40 basis points. In terms of the current interest rate difference in the national debt period, the 5Y-3Y spread spread and the rest narrowed (compared with March 31).

In response to the MPA assessment in the first quarter and the liquidity problem at the end of the quarter, the issuance of interbank deposits in February and March 2017 reached a record high, and the issuance rate rose. At the end of March 2017, the stock of interbank deposits was 78,425.3 billion yuan, compared with the end of 2016. The scale is expanded by about 25%. If the market interest rate rises, the financing cost of the issuer of the deposit will be greatly increased, thereby aggravating the mismatch of funds (short-term deposit receipts and long-term interbank financial management and foreign bonds), resulting in the gradual expansion of risk correlation within the financial system. Therefore, the CBRC issued a series of documents for the interbank business at the time of the issuance of the deposit slip. The regulatory direction includes inter-bank financing at the debt side and bond investment at the asset end, and the leverage is increasing. On the debt side, inter-bank deposit receipts may be transferred from the bonds payable to inter-bank liabilities, which will have a greater restriction on the commercial banks and rural commercial banks that rely on the issuance of inter-bank certificates of deposit. On the asset side, the state-owned banks have begun to take the initiative. Contracting out-of-contract scales, if formed in a concentrated manner, will put pressure on the bond market.

In the overseas market, the Fed's series of views reflect its imperative attitude towards the contract reduction plan. With its continuous appeasement in the market, the process of shrinking the table is likely to proceed in a gentle and gradual manner. During the period, the Federal Reserve will continue to evaluate the impact of measures such as interest rate hikes and contract reductions on the global market; the “Study Conference†reached a consensus that the two sides agreed to conduct a “100-day plan†for trade negotiations, and the possibility of a large-scale trade war between China and the United States Lower; the United Kingdom plans to conduct general elections on June 8th, to unite the parliament as soon as possible and to consolidate the status of the ruling party; the first round of the French election, Mark Long has a higher rate than Le Pen, and the poll shows that Mark Long’s probability is in the second round. In the election, Le Pen was defeated. The political risk in Europe temporarily subsided. The rules of the Trump tax reform plan were in line with market expectations, but the details have not yet been announced.

In the first quarter, the overall performance of domestic economic data exceeded market expectations. GDP increased by 6.9% year-on-year. The added value of industrial enterprises above designated size increased by 6.8% year-on-year. Real estate development investment increased by 9.1% year-on-year, and urban fixed asset investment was 9.2%. However, infrastructure construction in fixed asset investment fell by 2.59% year-on-year in March, and the growth rate of commercial housing sales fell below 20% year-on-year. The sustainability of economic growth is questionable. In March, CPI rose by 0.9% year-on-year. The decline in food prices continued. Fresh vegetables, eggs, and livestock meat all declined to varying degrees. With the sluggish demand from consumers, the pig price continued to be weak in April. It is expected that CPI will remain at 2 in April. Below the %; March PPI rose by 7.6% year-on-year, but fell slightly but remained at a high level. The mining industry's growth rate in production data reached 33.7% year-on-year. However, the overall decline in bulk commodities in April may further fall.

|

![[Monthly report - financial futures] The net value of the portfolio is slightly retraced, and the CVaR portfolio performs better.](http://i.bosscdn.com/blog/fb/9d/95/307adf21d035c61f21236496f8.jpg)

|

![[Monthly report - financial futures] The net value of the portfolio is slightly retraced, and the CVaR portfolio performs better.](http://i.bosscdn.com/blog/0a/79/97/b9dd6c709451ec32c3dc001834.jpg)

|

![[Monthly report - financial futures] The net value of the portfolio is slightly retraced, and the CVaR portfolio performs better.](http://i.bosscdn.com/blog/8d/2f/ab/9cf8d7a583459c92015a3bef48.jpg)

Commodity:

Gold: In late March, the US Health Insurance Law voted to cancel the vote. Trump announced that he would not consider abolishing Obama's medical insurance for the time being, turning the policy focus to tax reform, the policy progress is slow, and the risk assets are generally adjusted, but the US durable goods orders and consumer confidence. The real estate data performed well. The GDP revision in the fourth quarter of 16 years also confirmed the strength of the US economy. The price of gold entered the April with a turbulent trend; in the case of the Russian subway bombing, the US military strike against Syria and Afghanistan, and the North Korean nuclear issue, Superimposed March non-agricultural data was less than expected, gold was greatly boosted; Paris gun case raised the uncertainty of the election, but the first round of results was shocking and the results of the second round of polls led to a decline in market risk aversion, a sharp correction in gold . The European and Japanese central bank interest rate meeting resolutions have chosen to stand still.

Crude oil: The oil price in the current period was first raised and then suppressed. The increase in the operating rate of the refinery in early April led to a slight decline in API crude oil inventories, and the destocking of refined oil products also provided support for the rise in oil prices. However, the EIA inventory data released afterwards is contrary to the fact that Syria’s air strikes have caused a risk of disruption of crude oil supply in the Middle East, but it is not a major oil producer, and the increase is limited. In the week of April 14th, EIA inventory data triggered a sharp drop in the oil market. Under the expectation of seasonal warming and improved downstream demand, gasoline inventories increased at a sequential rate. In addition, US domestic crude oil production rose for 9 consecutive weeks, worried about both sides of supply and demand. Curb the rebound in oil prices. In view of the market's most concerned reduction in production, the key is the decline in inventory. The overall implementation rate of cuts in OPEC countries participating in production cuts in March was down from February.

Metals: The concept of the early Xiong'an and the Australian hurricane pushed up the black line, but the pressure from oversupply forced the market to move into the downtrend channel. At the beginning of the month, the weekly blast furnace operating rate rebounded slightly, but in March the steel industry PMI finished product inventory index showed an expansion trend, indicating that downstream demand in March was less than expected. In mid-April, the decline in steel social inventories increased, signs of improvement appeared on the demand side, and the short-term decline in steel prices slowed down. In the case of non-ferrous metals, the concept of the Xiongan concept lifted the colored futures price at the beginning of the month, and the loosening of the Indonesian nickel export ban on nickel prices The Grasberg copper mine gradually resumed production and moderately eased the market's concerns about copper supply. Although the overseas supply side still has interference incidents, the trend of the copper market still needs to consider the impact of slowing demand. The expectation of the reform of the supply side of electrolytic aluminum continues to heat up, the restrictions on production in the Ministry of Environmental Protection's government regulations, and the construction project of the Changji People's Government of Xinjiang shut down 2 million tons of capacity on April 15 to support the aluminum price.

|

|

![[Monthly report - financial futures] The net value of the portfolio is slightly retraced, and the CVaR portfolio performs better.](http://i.bosscdn.com/blog/cd/45/61/08ef839a3586d6ddd2e48b811b.jpg)

|

![[Monthly report - financial futures] The net value of the portfolio is slightly retraced, and the CVaR portfolio performs better.](http://i.bosscdn.com/blog/e9/60/a7/e0bd17a795c3038eb009e4a373.jpg)

2, asset allocation model performance

In the "Asset Allocation Research Series: Application of Risk Parity Model and Conditional Risk Value Model", the validity of the risk assessment model and the conditional risk value model have been verified, and the risk parity model is more suitable for investors with lower risk preference. The adjustment of the conditional risk value model scheme is more flexible.

2.1 , risk parity model

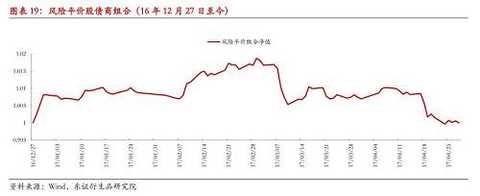

From the end of 16 years to the present, the risk-equity bond-debt portfolio has risen rapidly, but after experiencing the March 2016 agricultural product price of 000,061, the price of the stock market fell sharply, and the domestic stock price of this month fell across the board, the risk parity model established. The combined net worth has been substantially retraced, and all the increases at the beginning of the year have all been retreated.

|

Judging from the income evaluation indicators of the risk-equity bond-debtor portfolio, the largest retracement from the year-to-date is 1.87%, which is still higher than the maximum retracement of 1.31% in the previous month. Due to the poor performance of the net value this month, the Sharpe rate and the yield-to-risk ratio of the year-to-date performance are also poor.

|

Judging from the contribution of each target to the combined yield, crude oil, non-ferrous metals and government bonds are the main reasons for the sharp decline in this month's portfolio. The direct net loss caused by the three reached 0.14%, 0.25% and 0.47% respectively. The best performing asset is the Dow Jones Index, but it only reduces the net loss of this portfolio by 0.16%.

|

In terms of weight distribution, according to the risk parity model, the latest asset allocation plan for this month is smaller than the previous month, and only one target has a change of more than 1%. Among the commodity assets, the proportion of the allocation of precious metals and cotton candy index increased by 0.28% and 0.14%, respectively, while the proportion of non-ferrous metals decreased by 0.13%, and the other varieties were only slightly adjusted. The decline in the proportion of national debt allocation was the largest among all assets, reaching -1.11%. The proportion of funds allocated to equity assets continued to rise. The proportion of Dow Jones's allocation increased by 0.51%, which was relatively significant.

In general, because the risk parity model is the only basis for the allocation of funds with volatility, the government with the lowest volatility still accounts for the majority of the portfolio. In the asset allocation plan next month, investors are advised to continue to reduce the proportion of funds allocated to bonds and try to increase the allocation ratio of cotton, precious metals and equity assets.

|

2.2

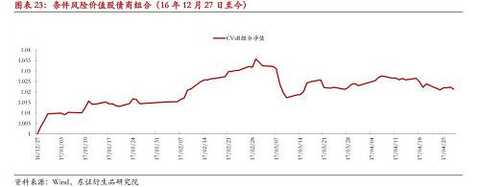

Conditional risk value modelFrom the end of 16 years to the present, the combination of conditional risk value bond dealers also rose rapidly. However, as the price of the bond dealers fell at the same time this month, the combination also showed a slight retracement, but the retracement was significantly smaller than the risk parity combination. From the performance of the year-to-date, the performance of this configuration scheme is more stable.

|

According to the income evaluation index of the conditional risk value debt bond combination, the maximum retracement from the year-to-date is 1.79%, and the maximum retracement occurred this month is 0.55%, which is only half of the risk parity model. From the performance of the year-to-date, the performance of this combination is still good. However, in the income evaluation indicators of the month, the Sharpe rate and the income risk ratio were affected by the sharp decline in the annualized rate of return of the month, and there was a large negative value.

|

Judging from the contribution of each target to the combined rate of return, the decline in the total wealth index of China Bond National Debt is the main reason for the slight decline in this month's portfolio. The direct net loss caused by it reached 0.43%. The best-performing asset is the Dow Jones Index, which reduces the net loss of this portfolio by 0.24%.

|

![[Monthly report - financial futures] The net value of the portfolio is slightly retraced, and the CVaR portfolio performs better.](http://i.bosscdn.com/blog/a7/3f/1a/efd64c76e524b511e9d3c00a5c.jpg)

In terms of weight distribution, according to the conditional risk value model, the latest asset allocation plan for this month is smaller than the previous month. Among the commodity assets, the proportion of each target is increased or decreased, and the precious metals, oil and agricultural products indices have been increased, and the ratio of their allocation to commodities has been reduced. The proportion of the allocation of national debt has risen by 2.99%. Although the total wealth index of the China Bond National Debt has performed poorly this month, according to the model, the tail risk of the index is relatively small, so the index is obtained in the portfolio of next month. A large increase in positions. The allocation ratio of equity assets declined, especially the proportion of CSI 300 decreased by 2.98%.

In general, in the portfolio of assets with tail risk as the basis for fund allocation, the government bonds with the lowest tail risk also account for the majority of the portfolio. In the asset allocation plan for next month, investors are advised to reduce the allocation ratio of non-ferrous metals and equity assets and re-allocate the allocated funds to precious metals, crude oil and national debt.

|

(Editor: Chen Hao HF072)

Woman'S Pants,Women Casual Pants,Women'S Trousers,Woman'S Straight Pants

Shaoxing Tongbang Textile Co.,Ltd. , https://www.sxtongbangtextiles.com